Executive summary

The April 2026 message for buyers of Brazil-origin ICUMSA 45 is straightforward: the screen is cheap, but execution is not. On the Intercontinental Exchange, Sugar No.11 is still trading at low nominal levels by recent standards, around 14.24 cents per pound on April 28, after touching a five-year low in mid-April. But No.11 is a raw sugar, FOB-origin benchmark. It is not a bankable, destination-specific CIF price for refined ICUMSA 45. ICE itself defines No.11 as raw cane sugar delivered FOB receiver’s vessel at origin, while ICE White Sugar is the benchmark for physical white sugar and specifies a maximum color of 45 ICUMSA at delivery. That structural difference is why the screen can look cheap while actual executable CIF numbers still feel expensive.

Primary-source crop signals from USDA Foreign Agricultural Service, CONAB, and UNICA point in the same direction. Brazil is not facing a cane collapse: FAS forecasts 2026/27 cane output at 675 million metric tons, up from 660 million, but expects mills to tilt the mix toward ethanol, with a 48% sugar / 52% ethanol split and total cane-sugar output at 42.5 MMT raw value, down about 3% year on year. That shift is being driven by policy and economics: the gasoline blend was raised from E27 to E30 in 2025, hydrous ethanol was compensating producers about 20% better than sugar by early 2026, and Brasília has been studying a move from E30 to E32. Conab’s April 2026 fourth survey still shows 2025/26 as a very large crop at 673.2 MMT of cane and 44.18 MMT of sugar, while UNICA’s center-south data through mid-March show ATR at 138.25 kg/ton and sugar production still historically large. In other words, Brazil has cane, but not all of that cane wants to become export sugar.

Outside Brazil, India remains the most important swing risk for near-term white sugar balance. Reuters reported that India’s 2025/26 sugar production was being revised down to about 28.5–29 MMT versus ISMA’s 30.95 MMT estimate, with traders doubting that the country would ship even half of its authorized export quota. Later in March, Reuters also reported that Indian mills were rushing export deals because of a weak rupee and higher global prices, but container availability was limited and freight rates were rising. Meanwhile, Thailand provides partial offset, but not a full safety buffer; official Thai guidance pointed to 10.3 MMT in 2025/26 and 10.0 MMT the following year, while separate Reuters reporting flagged disease pressure and crop switching risks into 2026/27. For buyers, that means flat price risk is only half the problem. The other half is availability of refined white sugar, freight timing, inspection integrity, and payment-bankability.

ICE No.11 and the screen behavior that matters to buyers

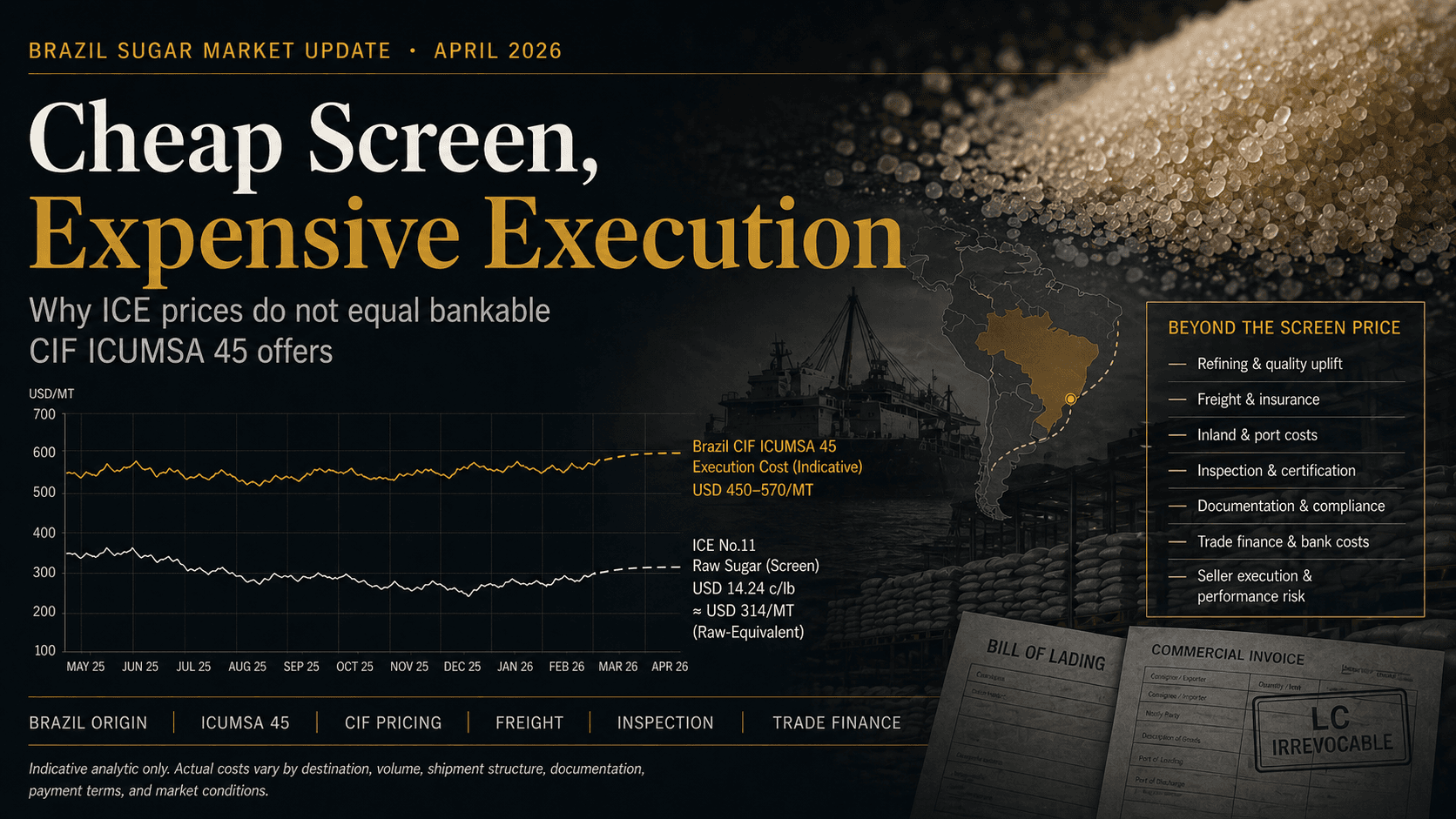

ICE states that Sugar No.11 is the world benchmark for raw sugar trading, sized at 112,000 pounds and quoted in cents per pound, with physical delivery FOB the receiver’s vessel at origin. As of April 28, public market references showed sugar around 14.24 cents per pound, equivalent to roughly $314 per metric ton in raw-equivalent terms. The recent trend has been highly event-driven rather than stable: sugar moved above 15.4 cents per pound in mid-March and early April as oil and ethanol economics tightened the market, then dropped to roughly 13.5–13.7 cents per pound by mid-April as ample near-term supply reasserted itself, before rebounding back above 14 cents by late April. The swing from about 15.4 to 13.66 cents per pound in roughly one month was more than 11%, which is substantial volatility for a buyer budgeting delivered food inputs.

The chart shown above converts the ICE raw sugar screen into $/MT raw-equivalent and overlays a stylized indicative Brazil CIF ICUMSA 45 midpoint. That CIF line is not a public offer feed; it is an analytical reconstruction using the futures checkpoints cited here and a midpoint basis uplift consistent with the white-sugar benchmark spread plus average logistics, inspection, freight, and finance costs. The point of the chart is not to claim a single executable number. It is to show why a “cheap” futures screen can coexist with materially higher delivered CIF economics.

A practical reading of the April tape is this: buyers should not chase every two- or three-point move in No.11 as if it were a one-for-one move in bankable CIF ICUMSA 45. In the current market, basis and execution variables are easily large enough to overwhelm a small move in the screen. That is the essence of “cheap screen, expensive execution.”

Physical ICUMSA 45 basis and the CIF cost stack

The first analytical mistake many buyers make is comparing Brazil CIF ICUMSA 45 directly to No.11 and stopping there. ICE White Sugar is the closer listed comparator, because ICE specifies it as the global benchmark for physical white sugar and allows a maximum color of 45 ICUMSA at delivery. In late April, white sugar references were around $418–427/MT while No.11 raw-equivalent values were around $301–314/MT, implying a raw-to-white inter-benchmark spread of roughly $110–120/MT before inland haulage, export handling, freight, marine insurance, inspection, and banking costs are added.

The right way to think about the “premium” on a Brazil CIF ICUMSA 45 offer is therefore not as one number, but as a stack: raw futures value, white/refining uplift, physical export logistics, marine transport, inspections, and performance-finance risk. When buyers ask for “best CIF,” what they are really asking for is the cheapest successful combination of those layers. In April 2026, that stack is still significantly above the raw screen even though the screen itself looks historically modest.

Brazil crop outlook and export availability

FAS forecasts Brazil’s 2026/27 cane crop at 675 MMT, with 620 MMT in the Center-South and 55 MMT in the North-Northeast. It expects better agricultural conditions than the prior cycle, with yield around 77.3 tons per hectare and total recoverable sugars around 138.2 kg per ton, but still projects lower sugar output because mills are expected to favor ethanol. FAS pegs the 2026/27 mix at 48% sugar and 52% ethanol and total cane-sugar output at 42.5 MMT raw value, versus 43.8 MMT in 2025/26. It also forecasts total sugar exports at 33.6 MMT raw value, including 29.5 MMT raw sugar and 4.1 MMT refined sugar.

The reason is economics, not agronomy alone. FAS reports that the mandatory anhydrous ethanol blend was increased from E27 to E30 in August 2025 and that hydrous ethanol was compensating producers about 20% more than sugar by the first quarter of 2026. The same report notes that the government had initiated studies on April 8 to raise the blend from E30 to E32 in the first half of 2026. Reuters separately reported that higher oil prices and stronger ethanol returns were expected to pull more cane toward biofuel, and Reuters later quoted the industry saying 2026/27 ethanol production could reach a record high. This is why better cane availability does not automatically translate into more export sugar.

Conab’s April 2026 fourth survey confirms that 2025/26 remained a very large supply year despite weather stress. It estimates 673.2 MMT of cane, harvested area of 8.95 million hectares, productivity of 75.184 t/ha, and sugar output of 44.176 MMT, described as the second-largest sugar output in its historical series. UNICA’s center-south industry data through March 16 show cumulative crushing of 603.67 MMT, average ATR at 138.25 kg/ton, sugar production at 40.25 MMT, and the sugar share of cane at 49.5%. The number differences between Conab and FAS are largely measurement and timing issues, including raw-value treatment, not a contradiction in direction. The common directional conclusion is that Brazil remains large, but the marginal 2026/27 increment is tilted toward ethanol rather than exportable sugar.

Harvest timing still matters operationally. FAS keeps the Center-South crop on its familiar April-to-March calendar, while the North-Northeast runs roughly September-to-August. For buyers, that means April and May are not just months of price watching; they are also months when rain, ramp-up efficiency, freight booking, and line-up management can still materially change execution quality for nearby shipments.

Global supply shocks beyond Brazil

India remains the most important external watchpoint because it affects nearby exportable white sugar supply and headline market sentiment. Reuters reported in February that India’s 2025/26 sugar production was likely to fall to roughly 28.5–29 MMT, below ISMA’s 30.95 MMT forecast, because excessive rainfall damaged yields across key producing states. Reuters also reported that even though India expanded the export quota to 2 MMT, traders doubted the country would ship even half of that amount, with some expecting exports not to exceed about 700,000 tons because domestic returns were more attractive. That is a meaningful support factor for nearby white sugar balance even in a world otherwise weighed down by larger supply.

The complication is that India can still influence sentiment even when actual shipped volume disappoints. Reuters reported in March that Indian mills were rushing export deals because the rupee had weakened and world prices had improved, yet container availability was limited and freight rates were rising. In other words, India can be “available on paper” while still being logistically constrained in practice. For importers, that means Indian news can swing the futures board without necessarily providing the physical relief buyers expect in delivered refined sugar.

Thailand is more of an offset than a shock, but it still matters. Public Reuters reporting through third-party republication showed Thailand expecting 10.3 MMT of sugar in 2025/26 and around 10.0 MMT the following year. At the same time, other Reuters coverage in late 2025 warned that cane disease and switching into cassava could drag 2026/27 production lower. This makes Thailand a stabilizer, but not a guaranteed surplus absorber if Brazil’s mix shifts further toward ethanol and India under-ships.

The European Union is also relevant because policy changes there can redirect Brazilian white sugar flows. Reuters reported in January that the European Commission planned to propose suspending the inward processing relief regime for some sugar imports, and follow-up Reuters coverage in March said that some duty-free imports were expected to be suspended for at least a year. That does not remove Brazil from the world market. It changes destination economics and can reshuffle which buyers get the most competitive origin attention. At the same time, market reporting from Bloomberg and the FAO-linked references picked up on the same March theme: white sugar was more sensitive than raw sugar to Middle East shipping and refining disruptions. For ICUMSA 45 buyers, that white-sugar sensitivity is more relevant than the raw board alone.

Freight, inspection, and trade finance

On freight, large-parcel sugar still behaves like a bulk commodity, while smaller bankable ICUMSA 45 programs are often handled in bagged or containerized form and inherit a different cost structure. That distinction matters. No.11 itself is a bulk, FOB-vessel benchmark, and the white sugar contract is also a physical FOB benchmark. By contrast, containerized or bagged CIF programs absorb box availability risk, higher per-ton freight, and more handling points. Public freight indicators show the environment is still not frictionless: Drewry’s World Container Index was $2,232 per 40-foot container on April 23 and still noted war-risk surcharges linked to Middle East disruptions; Freightos likewise described global ocean rates as elevated, even if mostly leveling off; and the Baltic Exchange dry bulk index hit a more-than-four-month high on April 17. Those are not Brazil sugar route quotes. They are the public benchmarks showing the direction of travel in the transport environment.

Brazil’s broader ag-export logistics also show why execution must be budgeted, not assumed. Reuters reported severe truck backlogs in northern export corridors during the soybean peak and separately reported that tighter export checks had lengthened waiting times for ships and pushed Panamax freight from the Port of Santos to major northern Asian ports about 24% higher in March in the soybean trade. That is not a sugar-specific freight quote, but it is an important signal: certification and port-system delays in Brazil’s agricultural complex can quickly convert into demurrage and higher freight, which ultimately feeds into sugar CIF numbers as well.

On inspection, buyers should think in terms of evidence continuity from load port to discharge port. SGS states that its agricultural loading and discharge supervision covers sampling, testing, quality, quantity and weight determination, packaging and label verification, sealing, traceability, and real-time reporting. SGS also offers draft survey services for quantity certification in bulk cargoes and tally services so that quantities on bills of lading and mate’s receipts are properly supported. For bagged sugar, tally and packaging-condition verification are especially important. For bulk sugar, draft survey, cleanliness, and sampling protocol discipline matter more. In both formats, the buyer should ensure that the contract clearly states which certificate prevails at load and how any discharge discrepancy is to be tested and claimed.

On payment structure, the distinction between a documentary credit and a standby credit is fundamental. The International Chamber of Commerce explains that documentary credits are a primary means of payment under UCP 600, while standby structures are secondary instruments governed more naturally by ISP98 or demand-guarantee logic. HSBC describes the LC as a cross-border payment assurance tool that pays against agreed conditions and shipping documents. Citibank describes standby products as covering non-performance, advance payment, bidding, and commercial payment default. For commodity CIF sugar, a sight irrevocable documentary LC usually gives cleaner payment mechanics than pretending an SBLC is the same thing. When issuer-bank or country-transfer risk is material, a confirmed LC can be worth the extra cost because it shifts payment risk away from the buyer’s issuing bank alone.

A typical documentary set for a Brazil CIF ICUMSA 45 cargo normally includes the signed commercial invoice, packing list, full set of clean on-board transport documents, certificate of origin, marine insurance certificate or policy, independent quality and quantity certificates, and any destination-specific sanitary, phytosanitary, fumigation, or conformity documents required by the importing country. SGS e-certificates are designed to be globally accepted by trade partners, banks, and financial institutions and to comply with eUCP rules. UCP 600 also makes clear that amendments cannot simply be imposed unilaterally; the issuing bank, confirming bank if any, and beneficiary must agree. That is why drafting discipline before opening the credit matters more than buyers often assume.

The CIF workflow below is a practical synthesis of Incoterms logic, UCP-style documentary practice, SBLC usage where applicable, and independent inspection sequencing. Actual contracts vary, but the gatekeeping points are always the same: bankability, inspection clarity, and documentary compatibility.

Execution risks, buyer checklist, and open questions

In the current market, the most common buyer error is not paying too much attention to price. It is paying too little attention to executable detail. A cheap CIF offer that cannot survive inspection, bank examination, freight booking, or documentary scrutiny is not a cheap offer. It is simply a failed transaction in disguise.

The red flags worth treating seriously are these:

- A seller quotes “ICE plus premium” but cannot explain whether that premium includes white-sugar uplift, freight, insurance, inspection, and bank costs.

- The loading port, shipment window, quantity tolerance, or packaging format are vague or left “to be advised.”

- The seller pushes an SBLC as if it were identical to a sight documentary LC.

- The issuing bank is not named early, or confirmation feasibility is never tested before the contract is signed.

- The inspection clause mentions quality but not quantity, tally, seals, packing condition, draft survey logic, or dispute methodology.

- The transport documents required under the credit are unrealistic, contradictory, or likely to create discrepancies at presentation.

- The number is materially below the analytical cost floor without any credible explanation tied to parcel size, destination, or payment structure.

Before requesting firm CIF quotes, a buyer should send a structured inquiry that includes the exact product specification, quantity and tolerance, intended shipment month or window, packaging requirement, discharge port and discharge capability, preferred payment instrument and issuing-bank shortlist, whether confirmation is required, the demanded documentary set, the inspection logic at load and discharge, the governing law or arbitration preference, and any destination-specific import certificates that must be bankable under the credit. In practice, the quality of the RFQ strongly determines the quality of the price received. A vague inquiry almost always produces either a fake number or a number padded with uncertainty premium.

Open questions and limitations

Because no buyer country was specified, all freight, insurance, and regulatory figures in this article are necessarily destination-agnostic bands rather than route-specific executable numbers. Public markets also do not provide a transparent, exchange-style live tape for bankable Brazil CIF ICUMSA 45, so the physical basis shown here is an analytical reconstruction from futures, public freight indicators, and standard execution costs. Any actual purchase decision should therefore narrow the analysis by destination, parcel mode, packaging, shipment month, and issuing bank before the credit is opened.

If you are buying ICUMSA 45 from Brazil in this market, the commercially correct next step is not to request the “lowest CIF” in isolation. It is to request a firm CIF quote with the full documentary schedule, named loading basis, shipment window, inspection clause, and acceptable bank structure attached. A serious seller should be able to issue a bankable draft contract and documentary list that can actually execute, not just a screen-linked headline number.