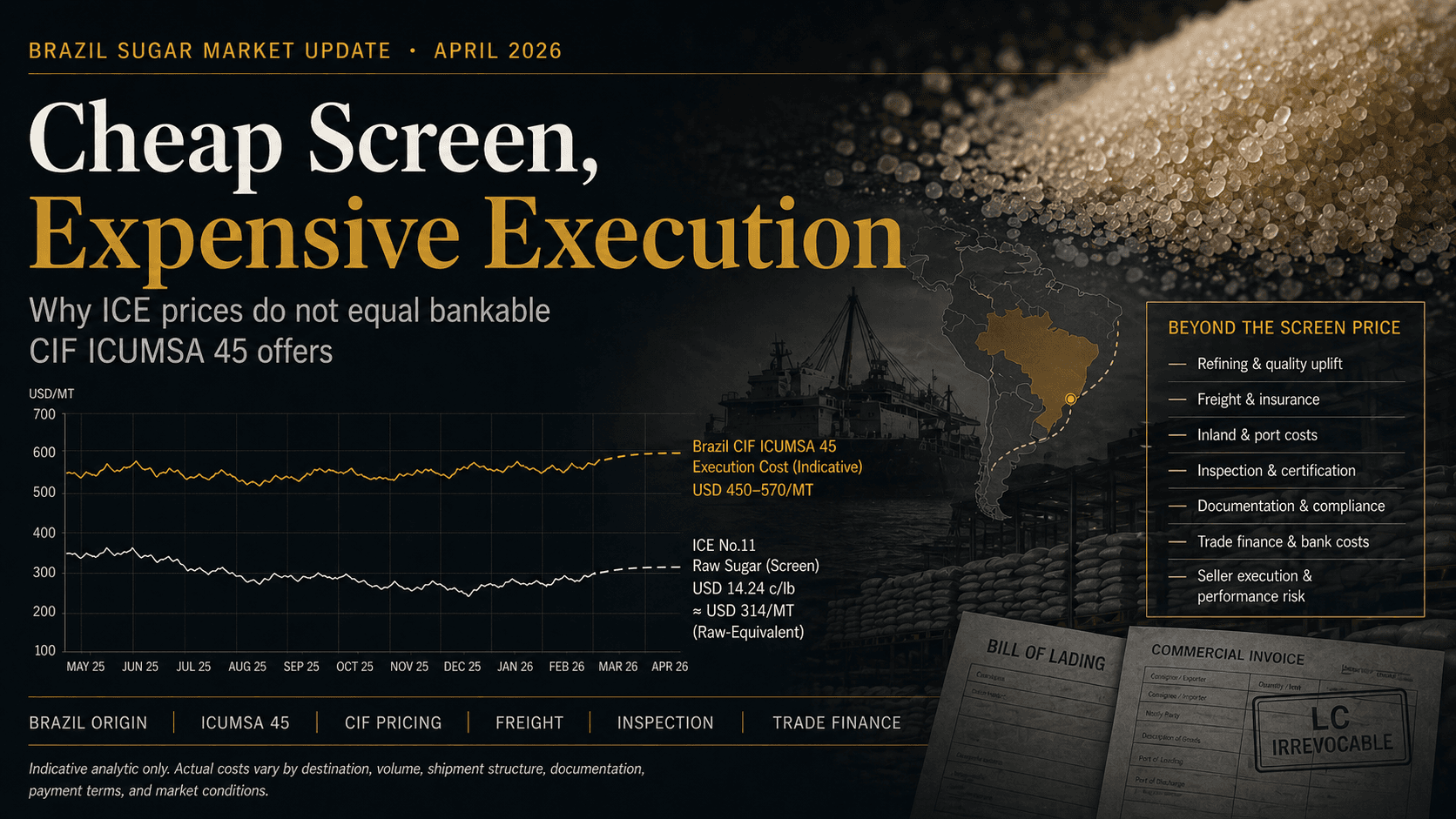

Brazil Sugar Market Update for April 2026

ICE sugar prices may look cheap, but Brazil-origin ICUMSA 45 CIF execution tells a different story. This update breaks down the real cost stack—refining uplift, freight, inspection, and trade finance—and explains why serious buyers must look beyond the screen.

Ler mais